How Algo Trading Creates Passive Returns for Retail Traders!

- Steven Hartwell

- Jun 5

- 8 min read

Updated: Jun 5

Algorithmic trading is defined as the automated execution of trades using predefined, rule-based instructions tied to price, timing, quantity, or mathematical models. Understanding how algo trading creates passive returns starts with recognizing that these systems remove the human from the decision loop, letting code handle entries, exits, and risk controls around the clock. The result is a trading process that generates returns with far less continuous manual intervention than traditional discretionary trading. Tools like bracket orders, automated signal platforms, and rules-based rebalancing systems make this possible for retail traders today, not just institutional desks. Passive here means reduced active management, not zero oversight.

How algo trading creates passive returns through automation

Algorithmic trading generates passive-like returns by replacing moment-to-moment human decisions with coded rules that execute automatically. Once a strategy is programmed, the system monitors markets, identifies conditions, and places orders without waiting for you to act. That shift from reactive to systematic is where the passive income potential lives.

The mechanics behind this break down into five core functions:

Emotion removal: Coded rules eliminate panic selling and FOMO buying, the two behaviors that most consistently destroy retail trader returns. A rule fires or it doesn’t. There is no hesitation.

Execution quality: Algorithms place orders at the best available price with low latency, reducing slippage and transaction costs compared to manual entry. Instant, accurate order placement across multiple conditions simultaneously is something no human trader can replicate.

Scheduled rebalancing: Rules-based systems can rebalance a portfolio on a fixed schedule, weekly or monthly, without requiring you to log in and make judgment calls. This is how factor ETFs operate, and it is directly applicable to retail algo setups.

Spread capture: Market-making algorithms earn returns by continuously quoting buy and sell prices and capturing the bid-ask spread, adjusting inventory risk algorithmically. This is a passive income source that runs as long as the system is live.

Broker-level risk controls: Bracket orders with stop-loss and take-profit levels enforce discipline server-side. A typical configuration might set a stop-loss at negative 2%, a take-profit at positive 8%, and a maximum 2% risk per trade, all enforced automatically through a broker API.

Pro Tip: Set your bracket orders at the broker level, not just inside your trading platform. Server-side enforcement means your risk limits hold even if your internet drops or your platform crashes.

How different algo strategies compare for generating passive income

Not all automated strategies produce the same type of passive return. The right choice depends on your risk tolerance, capital size, and how much monitoring you are willing to do.

Strategy | Passive income mechanism | Risk level | Monitoring required |

Factor ETFs | Rules-based rebalancing captures systematic risk premia | Low to medium | Quarterly |

Trend following | Captures directional momentum across asset classes | Medium | Weekly |

Mean reversion | Profits from price returning to statistical averages | Medium | Daily |

Options selling (covered calls, cash-secured puts) | Collects premium income systematically | Medium to high | Weekly |

Crypto grid bots | Buys low and sells high within a defined price range | High | Daily |

Market making | Captures bid-ask spread through continuous quoting | High | Continuous |

Factor ETFs and systematic strategies represent the most accessible entry point for retail traders because they package rules-based exposure into a product that rebalances automatically. The decision burden shifts from you to the algorithm. For traders who want more control, trend following and mean reversion strategies offer distinct profiles.

Trend following is historically stable across decades of data, performing well during sustained directional moves in equities, commodities, and forex. Mean reversion works best in range-bound markets and requires tighter monitoring because it bets against momentum. Different algo strategies carry distinct risk-return tradeoffs: options selling adds premium income but introduces assignment risk; crypto grid bots generate yield in sideways markets but can suffer significant losses in sharp directional moves.

The honest framing is this: every strategy on that list can produce passive returns, but none of them produces guaranteed returns. Automation scales your edge if you have one. It also scales your losses if you don’t.

What steps build a reliable passive algo trading system?

Building a system that generates passive returns reliably requires a structured process. Skipping steps here is where most retail traders lose money.

Define your strategy hypothesis. Write down exactly what market condition your algorithm exploits and why that condition should persist. A vague hypothesis produces a vague strategy that fails in live markets.

Source clean data. Use adjusted price data that accounts for splits, dividends, and corporate actions. Dirty data produces backtests that look great and trade terribly.

Backtest with realistic assumptions. Include transaction costs, slippage estimates, and bid-ask spread in every backtest. Strategies that fail realistic testing including transaction costs are the primary source of disappointment in algorithmic automation.

Run walk-forward analysis. Split your data into in-sample and out-of-sample periods. A strategy that only works on the data it was built on is not a strategy. It is curve-fitting.

Paper trade before going live. Paper trading with key metrics including win rate, Sharpe ratio, and maximum drawdown validates your strategy before real capital is at risk. Most serious retail projects enforce this gate before any live deployment.

Deploy with position sizing rules. Never risk more than a fixed percentage of capital per trade. Two percent per trade is the standard starting point for most systematic strategies.

Monitor continuously but not obsessively. Set alerts for drawdown thresholds and review performance weekly. Automation handles execution; you handle oversight.

Pro Tip: Use a systematic trading approach that includes both in-sample and out-of-sample validation before committing real capital. Strategies that pass both tests have a meaningfully higher probability of surviving live market conditions.

The most common mistake at this stage is skipping paper trading because the backtest looks strong. Backtests do not include execution risk, platform outages, or the psychological pressure of watching real money move. Paper trading does.

What are the real limitations of passive algo trading income?

Passive income from algo trading is real, but the word “passive” carries a misleading implication for many retail traders. Here is what the reality looks like.

Retail automation reduces manual trading time but does not eliminate risk or the need for ongoing monitoring. Bots require periodic review because model performance deteriorates as market regimes shift. A trend-following strategy that worked perfectly in 2023 may bleed steadily in a choppy, low-volatility environment in 2026.

The specific risks to understand before deploying any algo system include:

Model risk: Your algorithm is built on historical data. When market structure changes, the model’s assumptions may no longer hold. This is called regime change, and it is the most common cause of live strategy failure.

Platform and execution risk: Latency spikes, API outages, and slippage during high-volatility events can all erode returns. A strategy that looks profitable in backtesting may underperform in live execution due to these factors.

The “set and forget” misconception: No serious algo trader treats their system as truly hands-off. Weekly performance reviews, drawdown alerts, and periodic parameter updates are non-negotiable.

Scaling risk: A strategy that works with $10,000 may not work with $100,000 if it trades in low-liquidity markets. Market impact becomes a real cost at larger sizes.

Overfitting: Strategies optimized too tightly to historical data will fail in forward markets. The more parameters a model has, the higher the overfitting risk.

The passive income examples that actually work in systematic trading share one trait: they are built on simple, robust rules that survive across multiple market environments, not complex models tuned to a single historical period.

Key takeaways

Algorithmic trading creates passive returns by automating rule-based execution, removing emotional bias, and enforcing risk controls that run without continuous manual input.

Point | Details |

Automation removes emotion | Coded rules eliminate panic selling and FOMO, the two behaviors that most damage retail returns. |

Execution quality matters | Algorithms place orders faster and more accurately than manual trading, reducing slippage and costs. |

Strategy validation is non-negotiable | Walk-forward analysis and paper trading with Sharpe ratio and drawdown metrics must precede live deployment. |

Passive does not mean risk-free | Regime changes, model drift, and execution risk require ongoing weekly monitoring even in automated systems. |

Start simple and scale | Simple, robust rules outperform complex optimized models in live forward markets across asset classes. |

Why I think most retail traders misunderstand “passive” in algo trading

I have watched traders spend months building elaborate automated systems, then abandon them after the first drawdown because they expected the income to arrive like a dividend check. That expectation is the problem, not the technology.

The honest truth is that algorithmic trading creates a different kind of work, not less work. You move from staring at charts to reviewing performance logs, adjusting position sizing, and updating strategy parameters when market conditions shift. The emotional labor decreases significantly. The analytical labor does not.

What I have found genuinely valuable is the discipline that automation forces on you. When you have to write down your entry rules, your exit rules, and your risk limits in code, you cannot fudge them in the moment. That constraint alone produces better outcomes than most traders achieve through years of discretionary practice.

My advice for retail traders starting out: pick one strategy, keep it simple, and run it on paper for at least 60 days before risking real capital. Use automated risk controls like stop-loss and take-profit at the broker level from day one. The traders who build sustainable passive returns through algo systems are not the ones with the most sophisticated models. They are the ones who test rigorously, size positions conservatively, and treat monitoring as a professional obligation rather than an afterthought.

Patience and process beat complexity every time.

— James

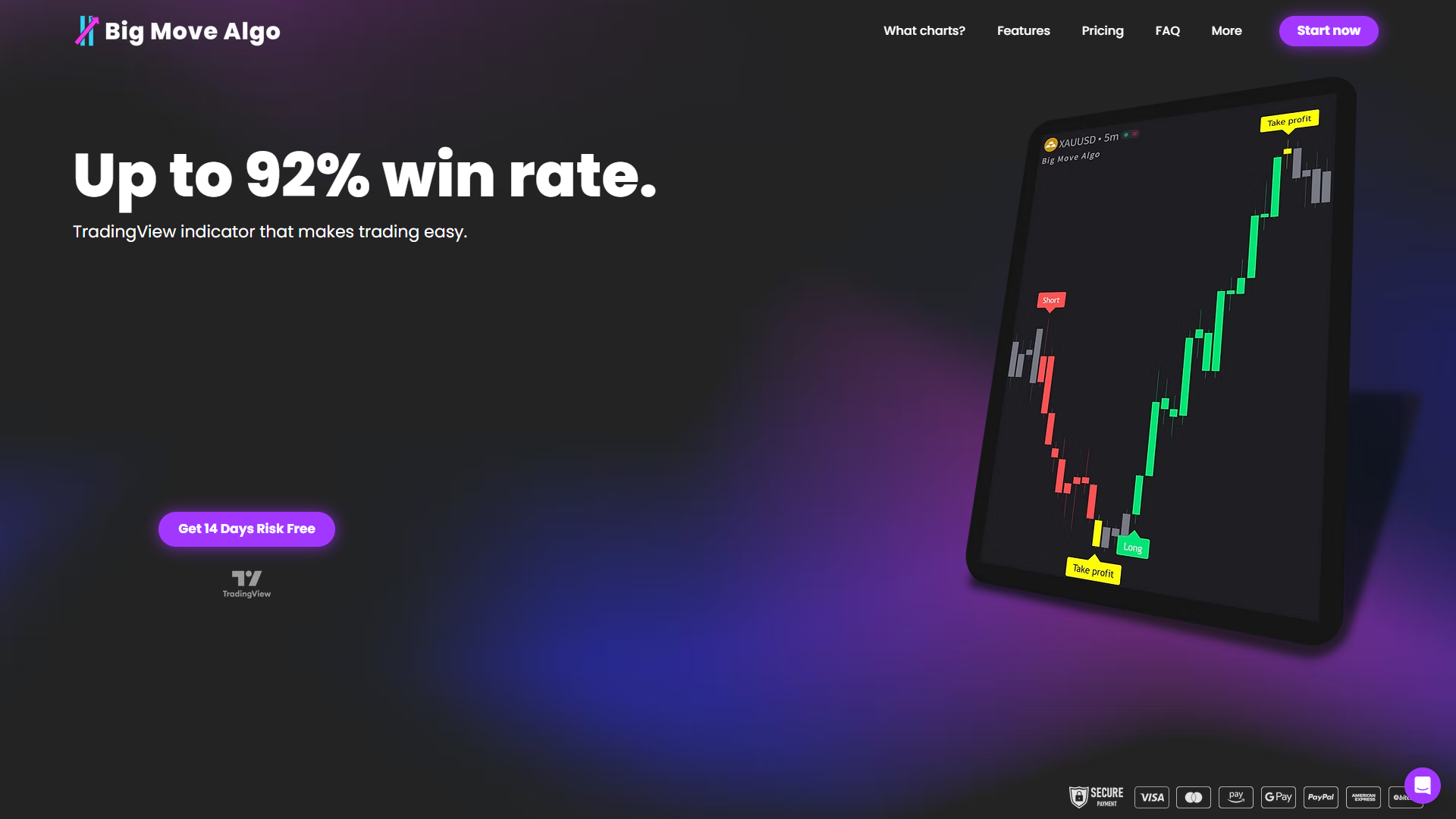

How Big Move Algo helps you build automated passive returns

If you are ready to move from theory to practice, Big Move Algo gives retail traders a direct path to automated, signal-driven trading without the complexity of building a system from scratch.

Big Move Algo is a TradingView indicator that delivers real-time Long, Short, and Exit signals across crypto, forex, stocks, indices, and commodities. The built-in Fake Trend Detector filters out low-quality market conditions before a signal fires, which means you are not trading noise. AUTO Mode gets you running with minimal setup, while Manual Mode lets experienced traders customize signal parameters. Combined with automated trade execution and the Big Move Guard risk controls, the platform handles the execution discipline that most retail traders struggle to maintain manually. Explore subscription plans and get instant access after purchase through Big Move Algo.

FAQ

What is passive income from algo trading?

Passive income from algo trading is returns generated by automated, rule-based systems that execute trades without continuous manual intervention. The income is “passive” in the sense that the algorithm handles execution, though ongoing monitoring and periodic adjustments are still required.

How do I start earning with algo trading as a beginner?

Start by defining a simple strategy hypothesis, backtesting it with realistic transaction costs, and paper trading for at least 60 days before deploying real capital. Validation metrics like win rate, Sharpe ratio, and maximum drawdown should all meet your targets before going live.

What are the main benefits of algorithmic trading over manual trading?

The primary benefits are emotion removal, faster and more accurate order execution, and the ability to run systematic strategies around the clock. Algorithmic execution also reduces transaction costs through better order timing and simultaneous multi-condition checks.

Can algo trading really be passive, or does it require constant attention?

Algo trading reduces active management significantly but is not truly “set and forget.” Bots require periodic review to catch model drift, regime changes, and execution issues. Weekly performance reviews and drawdown alerts are the minimum responsible oversight level.

Which algo trading strategy is best for consistent passive returns?

Factor ETFs and trend-following strategies offer the most historically stable passive return profiles for retail traders. Options selling adds premium income but requires more active risk management, while crypto grid bots work in sideways markets but carry higher volatility risk.

Recommended

Comments