What Is Algorithmic Trading? A Beginner's Guide

- Steven Hartwell

- Jun 9

- 8 min read

Algorithmic trading is defined as the use of computer programs that automatically execute buy and sell orders based on predefined rules and instructions, with no manual intervention required. Those instructions are built around quantifiable criteria: price levels, timing, volume thresholds, or mathematical models. The result is a trading process that operates faster than any human can react, removes emotional decision-making, and runs consistently across sessions. Platforms like TradingView and Interactive Brokers have made automated trading accessible to retail traders, not just institutional desks. If you want to understand how this works, what strategies it uses, and how to get started, this guide covers all of it.

What is algorithmic trading and how does it work?

Algorithmic trading, also called automated trading or algo trading, works by encoding a set of decision rules into a software program. When market conditions match those rules, the program places a trade automatically. A simple example: buy when a 50-day moving average crosses above a 200-day moving average, and sell when it crosses back below.

The system monitors live market data continuously, evaluates that data against its logic, and routes orders to the exchange in milliseconds. Execution speed in milliseconds is one of the defining advantages over manual trading, where even a fast human takes several seconds to recognize a signal and act. That gap matters enormously in liquid markets where prices shift in fractions of a second.

Automated trading rules also eliminate emotion-driven deviations from a plan. A human trader might hesitate on a valid signal because of a bad morning or override a stop-loss because of overconfidence. An algorithm does neither. It executes the rule, every time, without fatigue or fear. This consistency is what makes algorithmic trading attractive to both professional funds and individual traders learning to automate their strategies.

What are the main algorithmic trading strategies?

Common algorithmic trading strategy families include trend following, mean reversion, arbitrage, and market-making. Each operates on a different assumption about how prices behave, and each suits different market conditions.

Trend following is the most widely used approach for beginners. It assumes that assets in motion tend to stay in motion. Moving average crossovers, breakout signals, and momentum indicators are typical building blocks. The logic is simple: identify a trend early, ride it, and exit when momentum fades.

Mean reversion takes the opposite view. It assumes prices that move far from their historical average will return to it. When a stock drops sharply below its 20-day average, a mean reversion algorithm buys, expecting a bounce. This strategy works well in range-bound markets but fails badly in strong trending conditions.

Arbitrage exploits price differences for the same asset across different exchanges or related instruments. If Bitcoin trades at $65,000 on one exchange and $65,050 on another, an arbitrage algorithm buys low and sells high simultaneously. These gaps close in milliseconds, so speed is non-negotiable.

Market-making involves placing both buy and sell orders around the current price, profiting from the bid-ask spread. Market makers provide liquidity to the market and collect small profits on each transaction. This strategy requires significant capital and sophisticated execution infrastructure.

Strategy | Core logic | Best market condition |

Trend following | Ride directional momentum | Trending markets |

Mean reversion | Fade extreme price moves | Range-bound markets |

Arbitrage | Exploit cross-market price gaps | Any liquid market |

Market-making | Profit from bid-ask spread | High-volume, stable markets |

The right algorithmic trading strategy depends on your capital, risk tolerance, and the markets you trade. Most professional firms run multiple strategies simultaneously to reduce dependence on any single market condition.

What are the benefits and risks of algorithmic trading?

The benefits of algorithmic trading are concrete and measurable. Speed, consistency, and the removal of emotional bias are the three most cited advantages. Beyond those, algorithms can monitor dozens of instruments simultaneously, something no individual trader can do manually.

Key benefits:

Execution in milliseconds, far faster than manual order placement

Consistent rule application with no emotional override

Ability to backtest strategies on historical data before risking capital

Round-the-clock operation across global markets and time zones

Reduced transaction costs through precise order sizing and timing

Key risks:

Technical failures including connectivity loss, data feed errors, and software bugs

Overfitting during backtesting, where a strategy looks great historically but fails live

Flash crash exposure, where algorithms amplify volatility during market stress

Lack of human oversight during fast-moving, unusual market conditions

Regulatory scrutiny requiring documented controls and ongoing testing

Effective risk controls, compliance oversight, and ongoing testing are not optional. The UK’s Financial Conduct Authority has explicitly stated that pre-trade controls and resilient testing frameworks are required for firms running live algorithms. This expectation is spreading to retail platforms as well. Regulators also expect ongoing resilience verification through live environment testing, not just pre-deployment checks.

Pro Tip: Never run an algorithm without a kill switch. A kill switch is a manual override that halts all trading instantly. Even the best-designed systems encounter unexpected conditions, and the ability to stop everything in one action can prevent catastrophic losses.

How does an algorithmic trading system actually operate?

An algorithmic trading system is not a single program. It is a chain of interconnected modules, each handling a specific function. Modular system design isolates risks and allows targeted monitoring, so a data feed failure does not automatically corrupt your execution layer.

Module | Function | What can go wrong |

Data intake | Receives live price feeds and market data | Feed delays, corrupted data, gaps |

Signal generation | Applies strategy logic to incoming data | False signals, overfitted rules |

Risk management | Checks position limits and exposure | Misconfigured limits, ignored alerts |

Execution and order routing | Places and manages orders at the exchange | Slippage, partial fills, routing errors |

The data intake module pulls live prices, volume, and order book data from exchanges or data providers. The signal generation module applies your strategy rules to that data and produces a trade decision. The risk management module checks whether that trade is within your defined limits before it proceeds. The execution module then routes the order to the market using market orders, limit orders, or stop orders.

Execution quality often dominates over entry and exit logic in determining real-world performance. A strategy that looks excellent in backtesting can underperform live because of slippage, poor order routing, or execution timing. This is why professional algo traders spend as much time on execution infrastructure as on strategy development.

Pro Tip: When evaluating any algorithmic trading tool, ask specifically how it handles order execution and slippage. A tool that only shows entry and exit signals without addressing execution quality is giving you half the picture.

How can beginners get started with algorithmic trading?

Getting started with algorithmic trading does not require a computer science degree, but it does require a structured approach. Jumping straight into live trading with an untested algorithm is the fastest way to lose money. A step-by-step path reduces that risk significantly.

Here is a practical sequence for beginners:

Choose a platform with algo support. TradingView offers Pine Script for writing custom indicators and strategies. Interactive Brokers provides API access for Python and other languages. Both are widely used by retail algo traders.

Learn the basics of one programming language. Python is the industry standard for algorithmic trading strategy development. Its libraries, including Pandas, NumPy, and Backtrader, cover data analysis, backtesting, and live execution.

Define your strategy rules precisely. Vague rules cannot be coded. “Buy when the market looks strong” is not a rule. “Buy when the 10-period RSI crosses above 30 and price is above the 50-day moving average” is.

Backtest on historical data. Backtesting and paper trading validate strategy viability and expose implementation problems before you risk real capital. Use at least two to three years of data across different market conditions.

Paper trade before going live. Most platforms offer simulated trading environments. Run your algorithm in paper mode for at least four to six weeks to observe real-time behavior without financial risk.

Go live with strict position limits. Start with the smallest possible position size. Your goal in the first live phase is to confirm the system behaves as expected, not to maximize returns.

Individuals access algorithmic trading by programming their own strategies, purchasing commercial automated trading tools, or using broker platforms with built-in algo features. The build-versus-buy decision depends on your technical skills and how much customization you need. Commercial tools like Big Move Algo reduce the coding barrier significantly while still delivering structured, rules-based signals. You can review a platform checklist for new traders to evaluate your options before committing to any single tool.

Key takeaways

Algorithmic trading works because it replaces inconsistent human judgment with precise, repeatable rules executed at machine speed across any market condition.

Point | Details |

Core definition | Algorithms execute trades automatically based on predefined price, timing, or model-based rules. |

Strategy variety | Trend following, mean reversion, arbitrage, and market-making each suit different market conditions. |

Benefits of automation | Speed, consistency, and emotion removal are the primary advantages over manual trading. |

Risk controls are mandatory | Kill switches, position limits, and ongoing testing are required for safe live operation. |

Beginners should backtest first | Paper trading and historical backtesting must precede any live capital deployment. |

Why most beginners underestimate the execution layer

Most articles about algorithmic trading focus almost entirely on strategy logic. Pick the right indicator, code the right rule, and the profits follow. That framing is incomplete, and it leads beginners into a specific and expensive mistake.

The execution layer is where most real-world performance is won or lost. I have seen traders run strategies that performed beautifully in backtests, only to find that live slippage and poor order routing eroded every edge the strategy had. The signal was right. The execution was wrong. The account still lost money.

The second thing beginners consistently underestimate is monitoring. Automation does not mean set-and-forget. An algorithm running without oversight is a liability. Data feeds go stale. Market conditions shift outside the parameters the strategy was designed for. A system that worked for six months can start bleeding quietly if nobody is watching.

The honest truth about algorithmic trading for beginners is that the technology is now accessible, but the discipline required to use it well has not changed. You still need to understand what your system is doing and why. You still need to know when to override it. The traders who do well with automation are not the ones who trust it blindly. They are the ones who treat it as a tool that requires ongoing attention, not a passive income machine.

Start small. Test thoroughly. Monitor constantly. That is the actual learning curve nobody puts in the headline.

— Steven Hartwell

Take your first step with Big Move Algo

Understanding algorithmic trading is one thing. Having a tool that puts it to work for you is another.

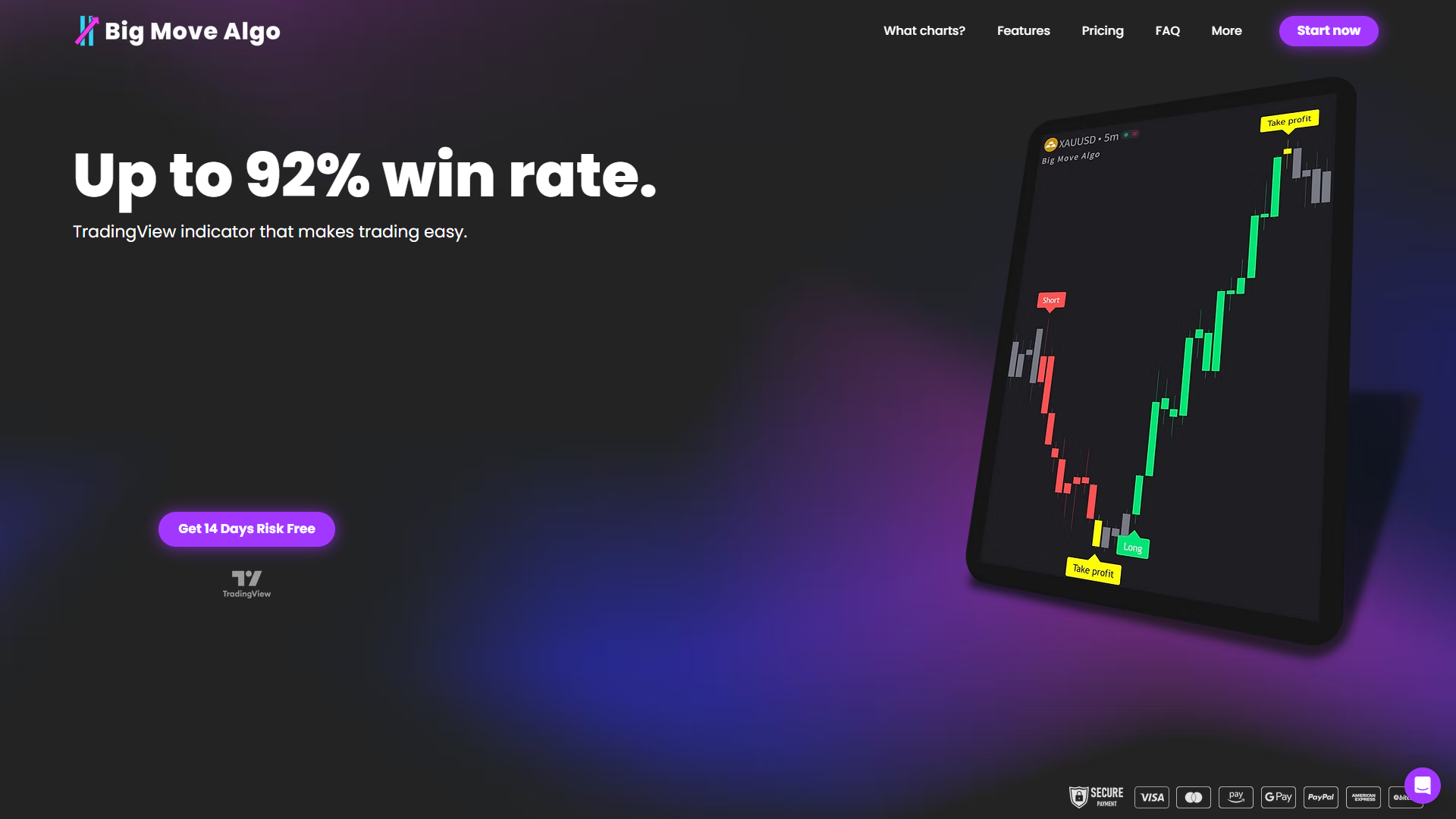

Big Move Algo is a TradingView indicator built for retail traders who want clear, rules-based signals without writing a single line of code. It delivers Long, Short, and Exit signals in real time across crypto, forex, stocks, indices, and commodities. The built-in Fake Trend Detector filters out low-quality market conditions so you are not trading noise. AUTO Mode gets you running in minutes, while Manual Mode gives experienced traders full customization. With up to 92% win rate signals and subscription plans designed for every level, it is one of the most direct ways to start investing with algorithms today. Explore the available plans and pricing to find the right fit.

FAQ

What is algorithmic trading in simple terms?

Algorithmic trading is the use of computer programs to automatically place trades based on predefined rules, such as price levels or timing conditions, without any manual input from the trader.

What programming language is used for algorithmic trading?

Python is the most widely used language for algorithmic trading strategy development, supported by libraries like Pandas, NumPy, and Backtrader for data analysis and backtesting.

Is algorithmic trading legal for retail traders?

Algorithmic trading is legal for retail traders in most jurisdictions. Regulatory bodies like the FCA require documented risk controls and ongoing testing for firms, and retail platforms increasingly apply similar standards.

How do I backtest an algorithmic trading strategy?

Backtesting runs your strategy rules against historical market data to measure how it would have performed. Platforms like TradingView and Interactive Brokers offer built-in backtesting tools, and Python libraries like Backtrader provide more advanced simulation pipelines.

Can I do algorithmic trading without coding?

Yes. Commercial tools and TradingView indicators like Big Move Algo provide rules-based trading signals without requiring any programming knowledge, making automated trading accessible to beginners.

Recommended

Comments